What's the Standard Annual Billing Discount for SaaS?

The standard SaaS annual billing discount is 15–17% — two months free. Here's the maths behind that number, why it almost always favours the business, and what it actually does to your churn and cash flow.

The standard SaaS annual billing discount is two months free; around 15 to 17 percent off the monthly rate. Most founders land on this without really knowing why, and some go higher thinking it'll convert more customers. Usually it doesn't, and the margin hit isn't worth it.

But the number only makes sense once you understand what you're getting in return. Annual billing isn't only a pricing tactic. It changes the economics of the business in ways that compound over time, and the discount is what makes the conversation possible.

You get the cash upfront

The case for annual billing starts here. When a customer pays annually, twelve months of revenue lands in your account immediately. For a small SaaS company, that's not just a nice number. It changes what you can do. You can hire knowing you can cover the cost. You can invest in the product without waiting to see what next month looks like. The anxiety of whether revenue will hold is a real drag on decision-making at an early stage, and annual billing reduces it in a way that monthly simply doesn't.

Annual customers churn less

This is the more important argument, and the one that doesn't get talked about enough.

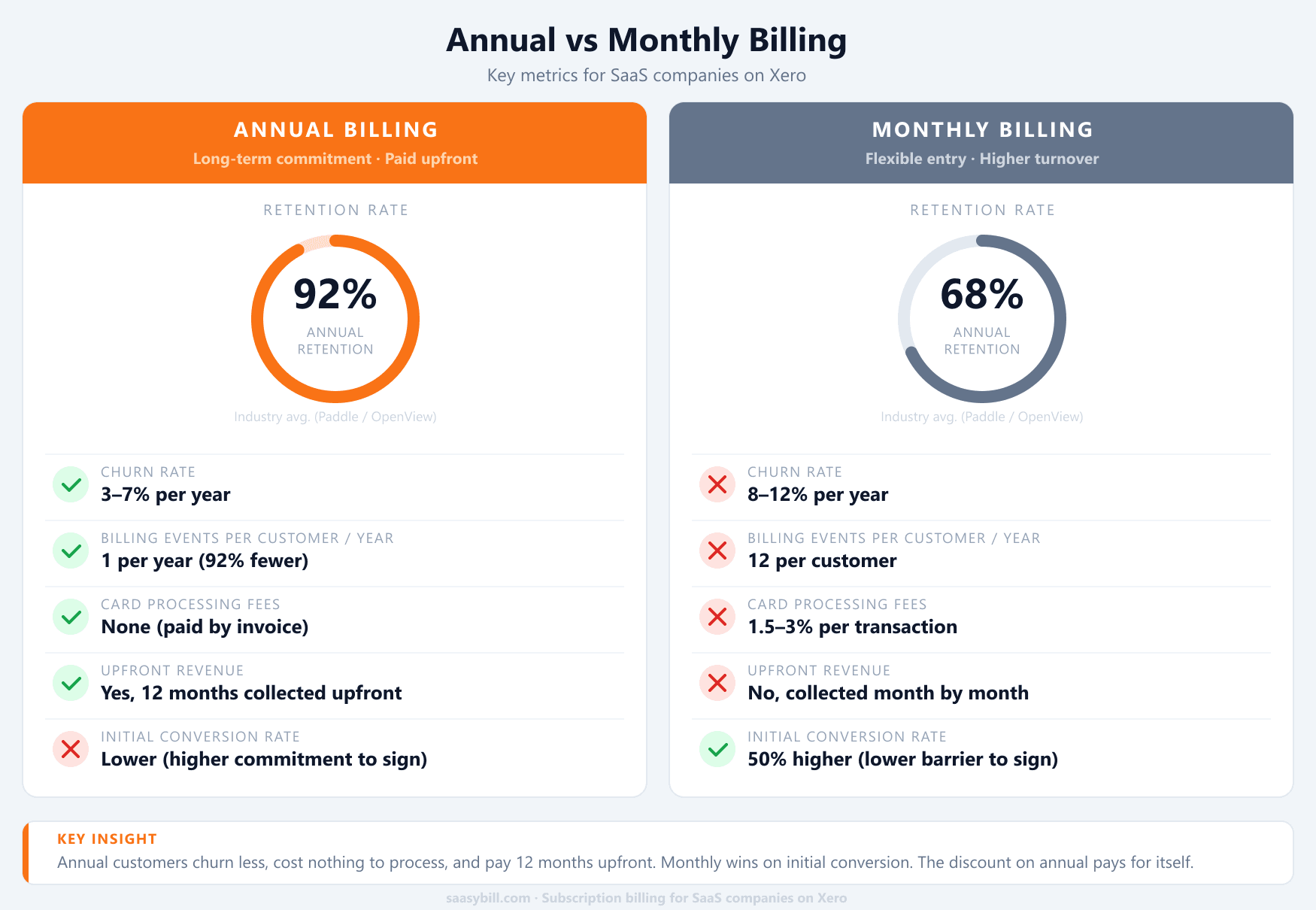

Annual customers churn at a significantly lower rate than monthly customers. The reason isn't complicated. When someone pays annually, they've made a real commitment. They're more likely to actually use the product, which means they get value from it, which means they renew. Monthly customers have an easy exit every 30 days. The low-friction cancellation that felt like a selling point when they signed up works against you every month they're slightly dissatisfied or just haven't got around to using the product properly. Annual customers have to actively decide to leave. Most don't.

Studies from Paddle and OpenView consistently show annual customers have 25 to 50 percent lower churn rates than monthly customers on equivalent products. Over a two or three year period, the lifetime value difference between a monthly and annual cohort is substantial, even after accounting for any discount you've offered to get them on annual.

You keep more of your revenue

Monthly billing almost always runs through a credit card, which means a payment processor takes a cut of every transaction, typically between 1.5 and 3 percent. On a $200 monthly plan that's not dramatic in isolation, but across 50 customers over a year it's decent money you're handing to a processor for the privilege of billing monthly. Annual billing paid by invoice through your accounting system sidesteps this entirely. One invoice, one bank transfer, no percentage skimmed off the top.

Then there's failed payments. Every billing cycle is an opportunity for a card to fail. Cards expire, limits get hit, details change after a replacement. Each failure creates admin, chasing, and the awkward experience of a customer losing access to something they're actively using. Annual billing doesn't eliminate this but it reduces your billing events per customer by 92 percent. If you have 50 customers on monthly plans, that's 600 billing events a year. On annual, it's 50. The surface area for things to go wrong shrinks dramatically.

The infographic below puts the key numbers side by side.

How to think about the discount

The standard framing is two months free, which works out to about 17 percent off. The maths almost always favours the business. You give up two months of revenue to get twelve months of cash upfront, a more committed customer, and significantly reduced churn. Going beyond 20 percent starts to erode margin without meaningfully changing conversion. If you're not sure where to start, 15 to 17 percent is a sensible default.

When to push it

None of this means you should force everyone onto annual. Early on, some customers won't commit to a product they haven't tried. Monthly removes that barrier and gets them in. The right approach is to offer both, make annual the more prominent option, and use the trial period to demonstrate enough value that the annual conversation is easy. For customers already on monthly plans, three to six months in is usually the right moment to bring it up. By then they're using the product, they know it works, and they're open to a conversation about locking in a discount.

The thing worth being deliberate about is actually having that conversation. Most SaaS founders don't. The monthly revenue keeps arriving and it feels like things are fine. But the customers who'd happily pay annually for a discount are also your lowest-churn customers. Letting them stay monthly indefinitely is leaving money on the table and accepting more churn risk than you need to.

Getting the billing set up properly

Once you start mixing annual and monthly plans, the operational complexity compounds quickly. Proration when someone upgrades mid-year, renewals landing at different times across your customer base, and making sure all of it lands in your accounting system correctly. If your Xero data is incomplete or inconsistent, the reporting you rely on stops being reliable. That's what I built Saasybill to handle. It sits alongside Xero and automates the invoicing, so annual and monthly plans, mid-cycle changes, and credit notes all get created directly in Xero without any manual work.

Get started

Start billing automatically in minutes.

Connect Xero, set up your plans, and have your first subscription running today. Every invoice lands directly in Xero. No spreadsheets, no sync errors.